What Is the 10-Year FIA + GLWB Runway Strategy Before Retirement?

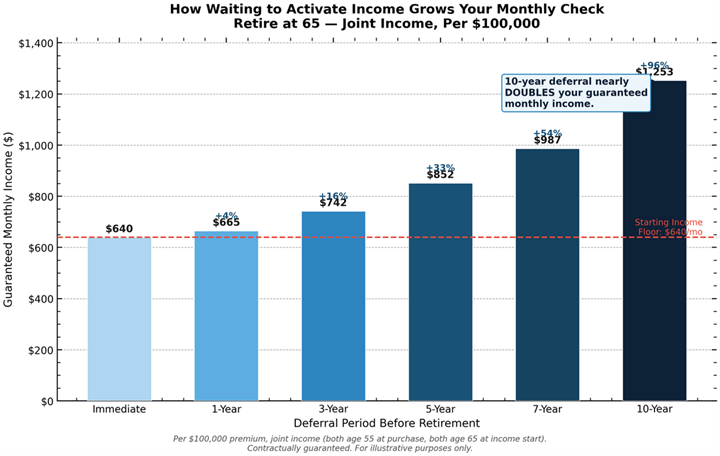

Funding a Fixed Indexed Annuity with a Guaranteed Lifetime Withdrawal Benefit up to 10 years before retirement can significantly increase your future guaranteed payout and income base, often producing much higher starting lifetime income than waiting until retirement to fund. A joint couple funding at age 55 and activating income at 65 can expect approximately $1,253 per month per $100,000 premium, compared to $640 per month for someone who funds and activates at 65. That is nearly double the guaranteed monthly income from the same premium, simply by starting sooner. The strategy preserves your account value and death benefit, gives you full flexibility on your income start date, and lets you know the exact contractually guaranteed income for every possible activation year before you commit to anything.

The runway is one lever inside a bigger plan. See the whole picture in your retirement paycheck.

How the 10-Year FIA + GLWB Runway Strategy Works

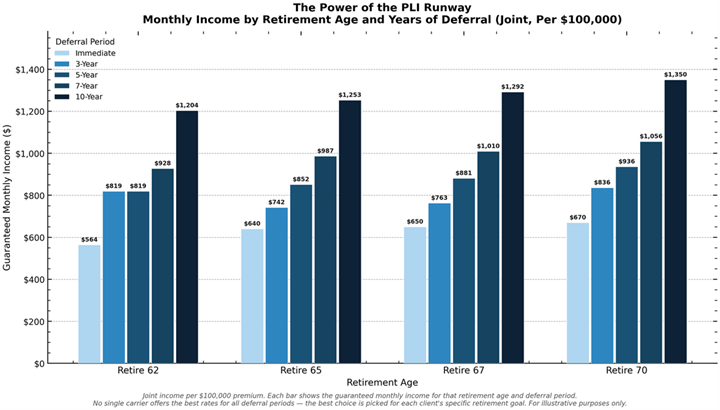

Most people think of annuities as something you fund at retirement when you need income to start. The runway strategy flips that assumption. Instead of waiting until your retirement date, you fund a FIA with GLWB up to 10 years before you plan to retire. During that deferral period, two things grow simultaneously: your income base, which grows at a contractually guaranteed rollup rate, and your payout factor, which increases the longer you defer. When you are ready to activate income, both of those numbers are significantly higher than they would have been if you had waited.

You do not have to decide your exact retirement date when you fund the strategy. Unlike a DIA, which requires you to lock in your income start date at purchase, a FIA with GLWB lets you choose when to activate income after the deferral period ends. You will know the exact guaranteed monthly income for every possible start date before you commit to anything. That flexibility is one of the most important advantages of this approach over other deferred income products.

The strategy becomes less efficient beyond 10 years for most designs, which is why the runway is framed as up to 10 years. Within that window, the earlier you fund, the more income you lock in for life.

Why Deferral Duration Dramatically Affects Your Guaranteed Income

The income difference between funding immediately at retirement versus funding 10 years earlier is not incremental. It is transformational. Here is why.

During the deferral period, your income base grows at a guaranteed rollup rate specified in the contract, typically between 6% and 8% per year depending on the carrier and product. That growth is not tied to market performance. It is contractually guaranteed. At the same time, your payout factor, the percentage of your income base you are guaranteed to withdraw each year for life, also increases the older you are when you activate income. Both the base and the percentage are growing simultaneously. The result is a compounding effect on your future guaranteed income that makes starting early significantly more powerful than waiting.

The Numbers: How Much More Income Does the Runway Produce?

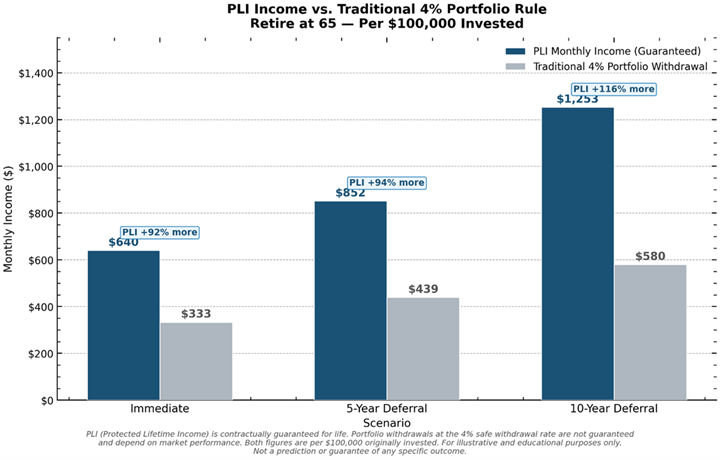

The table below compares guaranteed monthly income from a FIA with GLWB at different deferral periods against the equivalent monthly income from a traditional 4% portfolio withdrawal rule, all based on a $100,000 premium with income activating at age 65.

| Scenario | PLI Monthly Income | Portfolio 4% Rule | PLI Advantage |

|---|---|---|---|

| Immediate (fund and activate at age 65) | $640/mo | $333/mo | +$307/mo |

| 5-Year Runway (fund at 60, activate at 65) | $852/mo | $439/mo | +$413/mo |

| 10-Year Runway (fund at 55, activate at 65) | $1,253/mo | $580/mo | +$673/mo |

Based on $100,000 premium, joint male/female scenario, income activating at age 65. PLI figures are from actual carrier quotes as of 2026. Portfolio 4% Rule figures are hypothetical monthly equivalents of a 4% annual withdrawal from an account that grew at a hypothetical rate during the same deferral period. All figures are illustrative and for educational purposes only. Actual results will vary by age, health, carrier, product terms, and market conditions.

The 10-year runway produces $1,253 per month versus $640 for immediate funding, a 96% increase in guaranteed monthly income from the same $100,000 premium. Even a 5-year runway produces $852 per month, a 33% increase. And all three scenarios produce significantly more guaranteed income than the traditional 4% portfolio withdrawal rule, without any market dependence for the essential income floor.

How Deferral Boosts Your Guaranteed Income

Key Features of the 10-Year FIA + GLWB Runway Strategy

- Maximizes guaranteed income: Designed to produce the highest possible contractually guaranteed monthly income by the time you activate, particularly effective for joint couples who want both spouses covered for life.

- Preserves account value and death benefit: Unlike SPIAs or DIAs, your account value remains accessible subject to contract terms, and the remaining balance passes to your named beneficiaries at death.

- Flexible income start date: You do not lock in your retirement date years in advance. You fund the strategy now and choose your activation date when you are ready.

- Contractually guaranteed income for every start date: You know exactly what your monthly income will be for every possible activation year before you commit to anything.

- No forced annuitization: You maintain control and flexibility throughout the deferral period. You are not required to convert the contract to an annuity stream.

- Works with Roth, IRA, or after-tax dollars: Tax treatment depends on the funding source, giving you flexibility to fund from whatever account makes the most sense for your overall income plan.

- Can be laddered: You can fund multiple contracts in stages across different years to diversify your income start dates and build even more flexibility into your plan.

Who Is This Strategy Best Suited For?

- Pre-retirees between age 50 and 65 who want to maximize their future guaranteed income before they need it

- Couples who want the highest possible joint lifetime income with full flexibility on when to activate

- Anyone who wants to lock in income guarantees before retirement while keeping their options open on timing

- People who want to preserve account value access and a death benefit for heirs throughout the deferral period

- Those concerned about market risk, sequence of returns risk, or the possibility of outliving their savings

- Anyone eyeing an early exit, since this is exactly the runway a 55-year-old can use

- Anyone who wants to use Roth, IRA, or after-tax dollars strategically for income floor planning

How This Strategy Fits Into Lifestyle-First Planning

In a Lifestyle-First retirement income plan, the income floor covers your essential expenses and non-negotiable experiences with guaranteed income that markets cannot touch. The 10-year runway strategy is how you build that floor at the highest possible level for the least possible premium outlay.

By funding the FIA with GLWB a decade before you need income, you are essentially buying wholesale rather than retail. The same $100,000 premium that produces $640 per month at retirement produces $1,253 per month when funded 10 years earlier. That difference, $613 per month in additional guaranteed income, frees up more of your growth assets to remain invested for long-term purchasing power and legacy rather than being needed for essential expenses.

The runway strategy also pairs naturally with Social Security delay. If your essential expenses are partially covered by PLI income that has been growing for 10 years, you have more flexibility to delay Social Security to age 70 and lock in a permanently higher benefit. The two guaranteed income sources together, an optimized PLI floor and a maximized Social Security benefit, can create an income foundation that covers your essentials completely without any market dependence.

Myths and Truths About the 10-Year FIA + GLWB Runway Strategy

- Myth: You have to decide your exact retirement date right now to use this strategy.

Truth: You fund the strategy today and choose your income start date when you are ready. You will know the exact guaranteed monthly income for every possible activation year before you commit to anything. - Myth: Your money is locked away during the deferral period.

Truth: You retain access to your account value subject to contract terms and any applicable surrender charges. Your money is not inaccessible. - Myth: This strategy only works with traditional IRA dollars.

Truth: You can fund using Roth, IRA, or after-tax dollars. Tax treatment on the resulting income simply depends on the funding source. - Myth: If you pass away before activating income, the insurance company keeps your account value.

Truth: Your account value passes to your named beneficiaries. The death benefit is one of the most important advantages this strategy has over SPIAs and DIAs. - Myth: The income base growth during deferral depends on how well the market index performs.

Truth: For the highest-income designs, the income base grows at a contractually guaranteed rollup rate regardless of index performance. Your guaranteed income is not dependent on market returns during the deferral period. - Myth: All FIA with GLWB products offer the same runway benefits.

Truth: Payout rates, rollup rates, rider fees, and contract terms vary significantly between carriers. Always compare real current quotes before choosing a product.

Pros and Cons of the 10-Year FIA + GLWB Runway Strategy

Pros:

- Nearly double the guaranteed monthly income compared to funding at retirement using the same premium

- Full flexibility to choose your income start date without locking in years in advance

- Account value remains accessible and passes to heirs as a standard death benefit

- Income base growth during deferral is contractually guaranteed, not market dependent

- Works with Roth, IRA, or after-tax dollars for maximum planning flexibility

- No forced annuitization: you stay in control throughout the deferral period

- Can be laddered across multiple funding years or contracts for even more flexibility

Cons:

- Some products carry income rider fees and surrender charge periods that vary by carrier

- Guaranteed income amounts are based on contract terms, not actual account value growth or market performance

- Not all products or carriers are available in every state

- Guarantees rely entirely on the issuing insurer’s claims-paying ability

- May not be appropriate for those who need full liquidity or who do not expect to need guaranteed income in retirement

- Strategy becomes less efficient beyond 10 years for most product designs

Planning in Missouri, Florida, Kansas, Nebraska, and Iowa

The 10-year runway strategy works in all five states KJ Financial serves, but state rules affect how the income is taxed, what guaranty association protections apply, and which carrier products are available. Missouri, Florida, Kansas, Nebraska, and Iowa each have their own tax treatment rules for annuity income depending on the funding source, and guaranty association coverage limits vary by state. KJ Financial is licensed in all five states and builds runway strategies that account for your specific state’s rules alongside your overall income and tax plan.

Summary

The 10-year FIA + GLWB runway strategy is one of the most powerful tools available for maximizing guaranteed lifetime income well before you retire. By funding up to 10 years before your target retirement date, you can nearly double your guaranteed monthly income from the same premium, keep your income start date flexible, preserve your account value and death benefit, and know exactly what your income will be for every possible activation year before you commit to anything. For couples who want to protect both spouses for life and for anyone who wants to build the strongest possible income floor before markets can interfere, the runway strategy deserves serious consideration. Always compare real current quotes from multiple carriers before choosing a product, because payout rates and contract terms vary significantly.

Frequently Asked Questions

How does the runway strategy compare to a SPIA or DIA for deferred income?

A SPIA cannot be used for deferred income at all. It is an immediate income product only. A DIA allows deferral but requires you to lock in your income start date at purchase and surrenders your principal with no death benefit unless you add a rider. The FIA with GLWB runway strategy defers income like a DIA but gives you flexibility on the start date, preserves your account value, and includes a standard death benefit. And based on actual April 2026 quotes, the GLWB produces higher guaranteed income than the DIA at both 5-year and 10-year deferral periods.

Is the 10-year runway strategy right for everyone?

It is most appropriate for pre-retirees between age 50 and 65 who want to maximize future guaranteed income, preserve flexibility on their income start date, and build a Protected Lifetime Income floor before they need it. It is not appropriate for those who need full liquidity, those who do not plan to use the income in retirement, or those who expect to spend all assets before retirement. The fit depends on your specific age, health, funding source, and overall retirement income plan.

What is a Protected Lifetime Income floor and why does starting early matter so much?

A Protected Lifetime Income floor is a guaranteed income stream that covers your essential expenses regardless of market conditions. Starting early matters because both your income base and your payout factor grow during the deferral period, compounding your future guaranteed income in a way that cannot be replicated by waiting. The difference between funding at age 55 versus 65 can be nearly double the monthly income from the same premium, a gap that cannot be closed later without significantly more capital.

How does the runway strategy protect against sequence of returns risk?

By locking in a guaranteed income floor before you retire, the runway strategy ensures that essential expenses are covered by PLI income from day one of retirement. That means a market downturn in year one or two of retirement cannot force you to sell growth assets at depressed prices to pay your bills. Your income floor is already in place and fully funded. Your growth assets can stay invested and recover without being depleted at the worst possible time.

Does the runway strategy protect against inflation?

The guaranteed monthly income from a standard FIA with GLWB is fixed and does not automatically adjust for inflation unless you add a cost-of-living adjustment rider, which reduces the starting payout. In a Lifestyle-First plan, the growth asset layer handles long-term inflation protection. The spending smile concept also means your fixed PLI income often functions as a natural inflation hedge through your Slow-Go years when spending typically declines significantly from your Go-Go years.

How do Roth conversions interact with the runway strategy?

Funding the runway strategy with Roth dollars produces PLI income that is completely tax-free and does not count toward your MAGI for IRMAA purposes. Strategic Roth conversions in the years before you fund or activate your PLI strategy can significantly reduce the tax cost of future income. The combination of a Roth-funded runway strategy and strategic conversion planning before RMDs begin is one of the most powerful tax-optimization approaches available for pre-retirees.

How does the runway strategy interact with Social Security claiming timing?

When your essential expenses are partially or fully covered by PLI income that has been growing for 10 years, you have more flexibility to delay Social Security to age 70 and lock in a permanently higher benefit. A 10-year deferral from full retirement age to 70 increases your Social Security benefit by up to 32% permanently. Combining a maximized runway PLI strategy with a delayed Social Security claim can create an income floor that covers all your essentials with no market dependence at all.

Does PLI income from the runway strategy affect Medicare IRMAA surcharges?

It depends entirely on the funding source. Pre-tax funded PLI income counts as ordinary income and can push you into higher IRMAA brackets. After-tax funded PLI income uses an exclusion ratio where only the earnings portion is taxable. Roth-funded PLI income does not count toward MAGI and has no effect on IRMAA. Choosing the right funding source for your runway strategy is an important part of long-term Medicare cost management.

Does Missouri tax PLI income from the runway strategy?

As of 2026, Missouri fully exempts Social Security benefits from state income tax with no income limits. PLI income funded with pre-tax dollars is taxable as ordinary income at both the federal and Missouri state level. PLI income funded with after-tax or Roth dollars may have more favorable tax treatment depending on the funding source and structure.

Does Florida tax PLI income from the runway strategy?

Florida has no state income tax, making it one of the most favorable states for receiving PLI income from any funding source. Social Security, annuity income, and investment withdrawals are all completely free from state taxation in Florida.

Does Nebraska tax PLI income from the runway strategy?

As of tax year 2025, Nebraska fully exempts all Social Security benefits from state income tax with no income thresholds or phase-outs. PLI income funded with pre-tax dollars remains taxable at both the federal and Nebraska state level depending on the funding source.

Does Kansas tax PLI income from the runway strategy?

Kansas fully exempts all Social Security benefits for every resident effective tax year 2024, with no income threshold. Choosing between pre-tax and after-tax funding sources for a runway strategy still matters for Kansas retirees because it affects federal taxes and IRMAA, even though the state exemption is now automatic.

Does Iowa tax PLI income from the runway strategy?

Iowa does not tax Social Security for residents age 55 or older and also exempts most qualifying retirement income for eligible taxpayers. PLI income tax treatment in Iowa depends on the funding source and whether it qualifies as exempt retirement income under Iowa law.

Experience: Kurt H. Jackson has spent more than 16 years designing and implementing FIA with GLWB runway strategies for pre-retirees across Missouri, Nebraska, Kansas, Iowa, and Florida. He has worked directly with clients who came to him at age 62 or 63 wishing they had started a runway strategy 10 years earlier, and with clients at age 52 or 55 who used the strategy to lock in income levels at retirement that far exceeded what they could have achieved by waiting. Seeing the compounding difference firsthand in real client situations is what makes him one of the most vocal advocates for starting the runway as early as possible. Before founding KJ Financial, he spent 20 years as a Certified Mortgage Planner working with more than 1,000 clients on major long-term financial commitments.

Expertise: Kurt is a Retirement Lifestyle Architect and the creator of the Lifestyle-First Retirement Income Planning framework. He specializes in designing FIA with GLWB runway strategies that maximize guaranteed lifetime income for both singles and couples, coordinating income activation timing with Social Security delay, Roth conversion planning, and IRMAA management. He is Life and Health Insurance Licensed in MO, NE, KS, IA, and FL. His practice focuses exclusively on insurance-based, tax-optimized retirement income strategies. He does not manage investments or sell securities.

Authoritativeness: Kurt founded KJ Financial and operates MaxMyRetirementIncome.com as a dedicated educational resource for retirees and pre-retirees. The income figures on this page are drawn from real carrier quotes as of 2026, not industry averages or hypothetical projections. His ability to show clients side-by-side comparisons of immediate versus deferred activation using actual current quotes is what allows them to make genuinely informed decisions about when and how to fund their income floor.

Trustworthiness: KJ Financial is a compliance-first firm. All income figures on this page are based on real rounded-down quotes from actual carriers as of 2026 and are subject to change before contract lock-in. They are presented for educational comparison purposes only and do not represent a guarantee or offer. Kurt H. Jackson is not a securities broker, registered investment advisor, or CPA. Guarantees rely on the claims-paying ability of the issuing insurance company. State guaranty association coverage varies by state; check your state’s limits at nolhga.com.

Contact KJ Financial:

1014 E. 5th St., Maryville, MO 64468

Direct: 816.582.5532

Email: [email protected]

Website: www.MaxMyRetirementIncome.com

Educational only. Not tax, legal, or individualized investment advice. Guarantees rely on the issuing insurer’s claims-paying ability. Income figures shown are based on real rounded-down quotes from actual carriers as of 2026 and are subject to change before contract lock-in. Actual figures will differ based on age, health, carrier, product features, fees, and market conditions. State guaranty association coverage limits vary; see nolhga.com for your state’s details. Always consult a qualified financial, tax, or legal professional for your specific situation.