The Retirement You Already Paid For

Why the second way a retirement plan fails is the one nobody talks about, and why fixing it takes less than most people think.

Updated July 2026.

This page was reviewed and updated in July 2026. Two sections that were covered in more depth on a companion page were removed so each page does one job well, and this page now links across to that fuller discussion.

Direct Answer: What Is the Retirement Underspending Problem? Most people who saved carefully for retirement spend their years living well below what they could, and should, afford. They watch the market, worry about every drop, and quietly cancel the trips and experiences they spent decades working toward. Research from J.P. Morgan and BlackRock shows that retirees with guaranteed income spend 30% to 44% more than those without it. The difference is not the size of the account. It is whether the income is certain or merely probable. A plan built on probability produces anxiety. A plan built on a guaranteed floor produces freedom.

A woman came to me not long after she lost her husband. She was not a client when he was alive. She found me through a referral, and she was still grieving, the way you grieve when you have lost your partner of decades and suddenly have to figure out everything alone.

We talked about her finances. They were in reasonable shape. She would be okay. But at some point in the conversation she said something I have not forgotten.

“The most tragic thing,” she told me, “is that we worried so much about spending that we did not do the things we wanted to do.”

They had the money. They had the health, at least for a while. They had the trips they had always talked about. And they left them on the table, year after year, because every time they thought about spending, the market would move, the balance would dip, and the fear would win.

I asked what her advisor had been telling them. “Everything was fine,” she said. “We should have been comfortable.”

“So why did not you listen?”

“We just kept watching the balance go down every year. We did not know if it was going to come back.”

Here is the thing. Her advisor probably was not wrong. The math may well have worked out fine. But “the math says you are probably okay” is not the same thing as knowing the money is there. And no amount of probability closed that gap for them.

Her husband is gone. The trips are not coming back. That is the other way a retirement plan fails, and almost no one talks about it.

Two Ways a Retirement Plan Fails

The financial industry has spent fifty years terrifying people about one retirement risk: running out of money. It is the fear behind every Monte Carlo simulation, every “safe withdrawal rate,” every chart showing what happens if you live to 95 and the market has a bad decade.

That fear is legitimate. Running out of money in retirement is real and it happens. We take it seriously.

Here is something the industry will not tell you: not that many people actually run out of money in retirement. What happens is they get scared and either spend less on their own volition, or their advisor tells them to reduce spending. Sadly, they define you spending less and not running out of money as a successful retirement.

Would you define a retirement where you either felt you had to spend less, or were told you had to spend less to avoid running out of money, as a successful retirement?

But there is a second failure mode nobody mentions, because the industry has no financial incentive to. It looks like this:

You save your whole life. You do everything right. You retire with enough. And then you spend the next twenty years living like you do not have it, watching the business news every morning, stomach dropping every time the market moves, canceling the trips and the experiences and the time with the grandkids because the balance went down last quarter and you are not sure it is coming back.

That is not a market failure. That is a tool failure. And it is happening to a lot of people who would be shocked to hear that the research says they have more than enough.

The Tool Problem Nobody Explains

I have had clients come to me who were watching the business news constantly, anxious every time the market moved. When you ask what is really going on, they will tell you: they are afraid. They are uncertain. They have real anxiety about money they technically have.

I have seen this with people who are not even clients. You run into someone, ask how they are doing, and they mention they had plans to visit grandkids or go out but the markets were down so they just did not feel like they could do it. These are not people who are broke. These are people who saved, and it is not working the way they thought it would.

Here is why. A portfolio balance is a number that changes every single day. It goes up, it goes down, and every time it goes down, your brain registers it as a threat to your security. That is not an overreaction. That is a rational response to the tool you are using.

If your income depends on a balance that fluctuates, then every fluctuation is a legitimate threat to your income. Of course you watch it. Of course every drop triggers a recalculation. You are not doing anything wrong. The problem is the instrument.

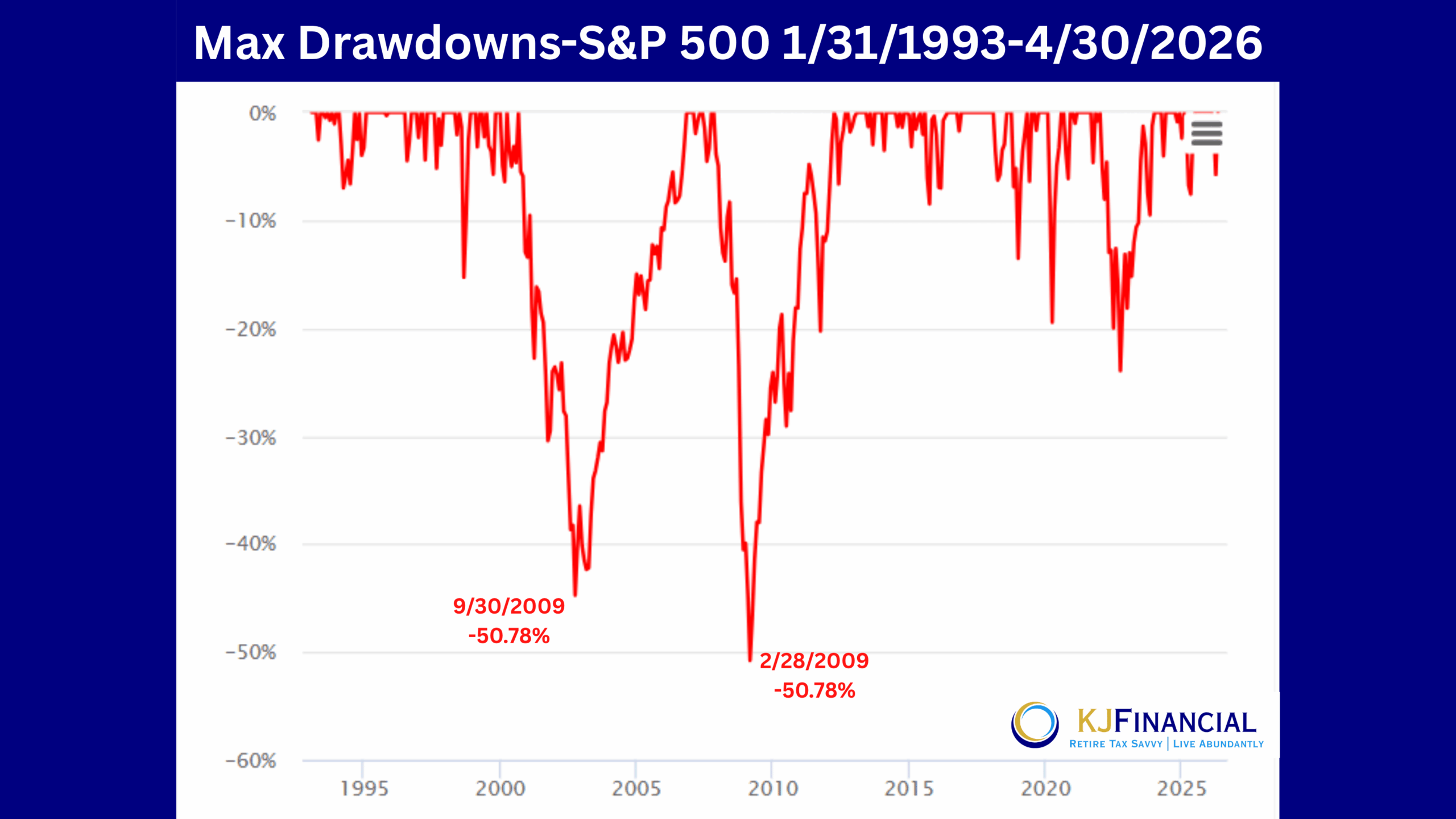

Here is what people are actually watching when they decide whether they can afford to visit their grandkids. The S&P 500 from 1993 through early 2026, showing how far it dropped from its peak at any given moment, including in years that finished positive.

Now ask yourself: does any amount of reassurance from an advisor fix that? Can “the math says you are probably okay” override what your nervous system is telling you every time the market drops three percent?

For most people, it cannot. And that is not a personal failing. It is a structural problem with a plan built on probability instead of certainty.

A Forecast Is Not a Plan

There is a tool sitting underneath almost every retirement plan you have ever been shown, and it is worth knowing what it actually is.

It is called a Monte Carlo simulation. Your advisor runs thousands of hypothetical scenarios and hands you back a score. Your plan has a 90% chance of success, something along those lines.

I have written separately about what a number like that does to a person, and why almost nobody hears the 90. That’s here: why so many retirees are afraid to spend money in retirement.

What I want to look at on this page is a different question. Whether a number like that can be trusted at all.

Advisors use language around these models that sounds like science. Alpha. Beta. Standard deviation. Probability-weighted outcomes. It sounds precise. It sounds certain.

It is not.

Think about it this way. If your granddaughter is getting married next June and she wants an outdoor ceremony, would you set the date based on a weather forecast? If it is a seven-day forecast, maybe. Those are reasonably accurate. But if someone handed you a forecast for a specific day fourteen months from now and said there is a 90% chance of beautiful weather, would you bet a wedding on it?

That is what a 30-year Monte Carlo simulation is. It is a forecast for a specific outcome more than three decades out, built on assumptions about market returns, inflation, interest rates, and your spending patterns that cannot possibly hold across that timeframe. It is a sophisticated guess dressed up as a projection.

And here is the detail that should give you pause: do you know who else uses Monte Carlo simulations? Las Vegas casinos. They use them to predict their win rate and your loss rate. Monte Carlo modeling was built to quantify the house’s advantage. When your advisor shows you a Monte Carlo result, ask yourself whose definition of success the model was built around.

I am not saying traditional planning never works. I am saying it works on probability, not certainty. And probability, no matter how favorable, cannot give you permission to actually spend your money.

What the Research Says About Guaranteed Income

This is not just an opinion. There is a body of academic research on exactly this question: do people with guaranteed income spend more than people without it? The answer, consistently, is yes. Significantly more.

J.P. Morgan’s research found that households with more guaranteed income as a share of their total retirement wealth spent meaningfully more in retirement. For people with between one and three million dollars in assets, moving from low to high guaranteed income share lifted median spending by 30% to 44%.

BlackRock found that embedding guaranteed income drove a 22% average increase in potential spending across all income levels.

David Blanchett, one of the leading retirement researchers in the country, called this the “license to spend.” The phrase is precise. It is not that people with annuities are reckless. It is that they have documented permission to spend what the floor covers, because the floor is certain. The market going down on a Tuesday does not change the number that hits their account on the first of the month.

Even Fidelity has said it plainly: a guaranteed income stream puts you “one step removed from the anxiety of watching the market.” That is not a pitch from someone selling annuities. That is a Wall Street firm acknowledging what the research shows.

The difference between a retiree who lives fully and one who does not usually is not the size of the account. It is whether the income underneath the lifestyle is certain or merely probable.

What This Looks Like in Real Life

Let me tell you about a couple I have worked with for more than a decade. When they first came to me, they had two things they were absolutely certain they did not want: an annuity and a reverse mortgage. Both were non-starters.

I sat down with them and showed them the numbers. They had a mortgage that was going to follow them well into their retirement years. The house had real equity, and their adult children, when I asked, told me clearly: they did not want the house. They wanted their parents to enjoy their retirement as much as possible.

A reverse mortgage eliminated their monthly payment. The property taxes, insurance, and upkeep stayed the same, but those are the same three things you would pay even if you owned the home free and clear. What changed was roughly $1,200 a month that was no longer leaving their account every month.

Then we took a portion of their portfolio and built a guaranteed lifetime income stream from it. Not all of it. A portion. Enough to create a floor under their lifestyle.

That was more than twelve years ago. They never had to touch the rest of the portfolio. They took trips. They saw their grandkids. They lived the retirement they had been building toward, because they knew every month what was coming in, no matter what the market did.

Her husband passed away not long ago. When I sat down with her and her children, her kids were understandably scared. Is Mom going to be okay? Is everything going to work?

The answer was yes. The plan had anticipated this moment. The floor was still there. The extra assets were intact if she ever needed them. She was, as I told her kids at that table, in great shape.

The widow’s tax situation, the bracket compression that hits surviving spouses, was more limited than it could have been because we had structured things to minimize it from the start. There is more on that in the Retirement Tax Avalanche.

That couple came to me resistant to both tools that ended up making the biggest difference. They left that first meeting skeptical. What changed was not the products. It was seeing how the pieces fit together into something they could actually feel safe inside.

That is what a floor really buys. Not a bigger number on a statement. The freedom to use the money while you are still well enough to enjoy it.

And that window is shorter than most people picture.[1] The years when you can take the trip, rent the beach house, fly out for a week with the grandchildren, those come at the front of retirement. They do not sit around waiting for the market to feel calm.

How We Build the Floor

What I do, and have done for more than fifteen years, is called Lifestyle-First Retirement Planning. It starts with a simple question: what does the retirement you actually want cost?

Not what does a safe withdrawal rate say you can spend. What does the life you built toward actually require, and what does it cost to make that certain rather than probable?

The answer, for most people, is less than they think. A Protected Lifetime Income Stack, combining Social Security timed correctly and a guaranteed income product purchased at the right time, can cover the essentials and the non-negotiables. The adventures. The experiences. The memories. The things worth doing while you still can.

It is even cheaper if you plan ahead up to about ten years before retiring, when guaranteed lifetime income is on sale, almost at clearance prices.

Once that floor is in place, the rest of the portfolio can be treated as what it actually is: long-term money. Not the thing standing between you and poverty. Not the balance you are watching every morning. Just money that can grow, because your lifestyle does not depend on it.

That is the difference between a 90% retirement and a certain one. And the certain one usually costs less to build than you would expect.

This may be a low blow, but it needs to be said. When you are gone, what do you want your grandkids to remember? The cruise you took them on, the weeks at the beach, the times you actually showed up. Or the check they got after the funeral. One of those creates stories they will tell their own grandkids. The other gets spent.

If you have been sitting on trips you keep postponing, watching the business news more than you would like to admit, or telling yourself “maybe next year” about things you actually want to do right now, it might be worth finding out whether your plan has a floor or just a forecast.

Frequently Asked Questions

What is retirement underspending?

Retirement underspending is when a retiree consistently spends significantly less than their plan allows, not because they lack money, but because they lack certainty that the money will last. Research shows it is one of the most common retirement outcomes and is directly linked to depending on a portfolio rather than a guaranteed income floor.

Why do people with enough money still feel like they cannot spend it?

Because a portfolio balance changes every day, and income that depends on a fluctuating balance feels permanently at risk. Every market drop is a legitimate threat to spending power when there is no guaranteed floor underneath it. The anxiety is not irrational. It is the correct response to the wrong tool.

What does research say about guaranteed income and retirement spending?

J.P. Morgan found that retirees with higher guaranteed income as a share of total wealth spent 30% to 44% more in retirement. BlackRock found a 22% average increase in spending when guaranteed income was embedded in the plan. Researcher David Blanchett called this the “license to spend”: when income is certain, people use it.

Is a Monte Carlo simulation an accurate retirement planning tool?

Monte Carlo simulations are probability tools. They show a range of possible outcomes based on historical data and assumptions. A 90% success rate means a 1-in-10 chance of failure is built into the plan, and the plan’s own definition of success includes the possibility of spending cuts. For a retirement lasting 25 to 35 years, that uncertainty is what drives the anxiety most retirees feel even when the math looks favorable.

What is Protected Lifetime Income and how does it create a floor?

Protected Lifetime Income is guaranteed income that continues for life regardless of market conditions, interest rates, or account balance. Combined with properly timed Social Security, it creates a floor under the retirement lifestyle: a known, certain monthly income that does not change when the market does. With a floor in place, the remaining portfolio can function as long-term money rather than a daily source of financial anxiety.

How do I know if my retirement plan has a floor or just a forecast?

Ask your advisor one question: what is the guaranteed component of my retirement income? Not the projected component, not the historically probable component. The guaranteed component. If the answer is only Social Security, your plan is built on a forecast. A Retirement Income Blueprint conversation can show you specifically what a floor would look like for your situation.

Does building a guaranteed income floor require giving up all my investments?

No. The goal is to use a portion of the portfolio to build a guaranteed income floor that covers the lifestyle, then let the remainder grow as true long-term money. Most clients are surprised at how little it takes to create meaningful certainty, particularly when income is built well before retirement begins.

How does the Tax Avalanche interact with the underspending problem?

The two problems compound each other. Retirees who underspend out of fear tend to leave large pre-tax balances intact, which grow the eventual Required Minimum Distribution burden, trigger Social Security taxation, raise Medicare premiums, and ultimately drop a concentrated tax bill on their children. Solving the underspending problem with a guaranteed floor also creates the opportunity to manage tax exposure strategically during the low-income window before RMDs begin. See the Retirement Tax Avalanche for a full explanation.

What is Lifestyle-First Retirement Planning?

Lifestyle-First Retirement Planning starts with the life you want, not with account balances or withdrawal rates. It identifies what the desired retirement lifestyle costs, builds a guaranteed income floor to make that lifestyle certain rather than probable, and then manages the remaining assets as long-term money. The goal is a retirement the client can actually live fully, not a plan optimized to maximize a portfolio balance at the end.

About Kurt H. Jackson, Retirement Lifestyle Architect

Experience

Kurt H. Jackson has spent more than 16 years working directly with retirees and pre-retirees in Missouri, Nebraska, Kansas, Iowa, and Florida. Before founding KJ Financial, he spent 20 years as a Certified Mortgage Planner working with more than 1,000 clients on major financial decisions. He watched clients lose money in the dot-com crash and saw the 2008 financial crisis hit families who had been told their plans were safe. That experience is what built his conviction that the retirement underspending problem is real, it is predictable, and it is preventable when you build a guaranteed floor before the fear sets in.

Expertise

Kurt is a Retirement Lifestyle Architect and the creator of the Lifestyle-First Retirement Income Planning framework. He is Life and Health Insurance Licensed in MO, NE, KS, IA, and FL. His practice focuses exclusively on insurance-based, tax-optimized retirement income strategies including Protected Lifetime Income design, Roth conversion planning, and the Retirement Tax Avalanche. He does not manage investments or sell securities.

Authoritativeness

Kurt founded KJ Financial and operates MaxMyRetirementIncome.com as a dedicated educational resource for retirees. His Lifestyle-First framework starts with the retirement the client actually wants, builds a guaranteed income floor to make it certain rather than probable, and manages the remaining assets as true long-term money. The research supporting this approach comes from J.P. Morgan, BlackRock, Morningstar, and peer-reviewed academic work by David Blanchett and Michael Finke. The framework connecting them is his.

Trustworthiness

KJ Financial is a compliance-first firm. All educational content on this page reflects current law and research as of 2026 and is subject to change. Kurt H. Jackson is not a securities broker, registered investment advisor, or CPA. Nothing on this page constitutes personalized tax or legal advice. Guaranteed income strategies involve real costs and require careful planning based on your individual circumstances.

Sources

- David Blanchett, “How Spending Evolves in Retirement: A Smile, a Smirk, or Something Else?” Financial Planning Review, 2026.

- Morningstar, retirement income research.

- BlackRock, guaranteed income and retirement spending research.

- Fidelity, “How to plan for rising health care costs.” fidelity.com

- Social Security Administration. ssa.gov

KJ Financial

1014 E. 5th St., Maryville, MO 64468

Direct: 816.582.5532

Email: [email protected]

Website: www.MaxMyRetirementIncome.com

Last updated: July 2026

This material is for educational purposes only and is not tax, legal, or investment advice. Tax rules are complex and change often, and everyone’s situation is different. The right approach for you depends on your specific circumstances. Please review any strategy with a qualified professional before acting. Guarantees related to any insurance-based strategies mentioned rely on the claims-paying ability of the issuing insurance company.

See it on your own numbers

Want to see your own Tax Avalanche?

A general warning is easy to wave off. Your own number is a lot harder to ignore. Put in a few rough figures and watch the cascade unfold, the withdrawal the government will force you to take, how much of your Social Security it can drag into being taxed, and what it can do to whichever spouse is left behind. It takes about two minutes, and you walk away with a one-page snapshot to keep.

Show me my Tax Avalanche