Are Annuities Ever a Fit for Retirement? Guaranteed Income, GLWB Rates and Trade-Offs 2026

Sometimes. Fixed indexed annuities with a Guaranteed Lifetime Withdrawal Benefit (GLWB) are the tool KJ Financial uses most often to create Protected Lifetime Income for retirement essentials. In 2026, a couple with the youngest spouse age 65 can expect approximately $640 per month per $100,000 invested, and a single age 65 approximately $690 per month per $100,000. These are illustrative rates subject to change before contract lock-in. The right fit depends on your income needs, timeline, liquidity requirements, and how much of your essential spending you want guaranteed for life regardless of what markets do.

What Is Protected Lifetime Income and When Does It Make Sense?

Protected Lifetime Income (PLI) is a guaranteed income stream designed to pay you a set amount every month for the rest of your life, regardless of market performance, interest rate changes, or how long you live. It is not a market investment. It is a contractual commitment from a highly rated insurance company.

PLI is not the right tool for every dollar or every goal. It is specifically designed to cover your essential expenses and the non-negotiable experiences that define your retirement lifestyle. Once those are secured with guaranteed income, the rest of your savings can be invested more aggressively for growth, flexibility, and legacy without the anxiety that comes from depending on markets for your basic needs.

The question is not whether annuities are good or bad in general. The question is whether a specific PLI solution, sized correctly for your essentials, improves your retirement income picture. In most cases we work through, the answer is yes.

Used this way, an income annuity becomes the engine behind your retirement paycheck, sized only to your essentials.

2026 PLI Payout Rates: What You Can Realistically Expect

The table below shows illustrative payout rates from current 2026 carrier data. Rates are subject to change before contract lock-in. Always verify current rates before making any decision.

| Solution Type | Who It Covers | Monthly Income per $100K | Annual Income per $100K | Effective Withdrawal Rate |

|---|---|---|---|---|

| FIA + GLWB | Couple (youngest spouse age 65) | $640 | $7,680 | 7.68% |

| FIA + GLWB | Single (age 65) | $690 | $8,280 | 8.28% |

| SPIA (life-only) | Single male (age 65) | $619 | $7,428 | 7.43% |

| SPIA (life-only) | Single female (age 65) | $598 | $7,176 | 7.18% |

Compare these to the traditional 4% rule, which produces $333 per month per $100,000, and the case for PLI becomes clear for retirees who want guaranteed income. A FIA with GLWB produces more than double that amount while keeping your account value accessible and preserving a death benefit for your beneficiaries.

Why FIA with GLWB Outperforms SPIA and DIA in Most Cases

Historically, Single Premium Immediate Annuities (SPIAs) and Deferred Income Annuities (DIAs) were the standard tools for guaranteed lifetime income. In 2026, fixed indexed annuities with a GLWB rider consistently outperform both in the scenarios we see most often, for several important reasons.

- A FIA with GLWB preserves your account value. If you pass away before depleting your account, the remaining balance goes to your beneficiaries. A life-only SPIA pays nothing at death.

- A FIA with GLWB gives you flexibility on when to start income. You can defer the start date and your income base continues to grow, often at a contractually guaranteed rollup rate. A SPIA starts paying immediately with no accumulation phase.

- A DIA allows deferral like a FIA, but also surrenders your principal with no remaining account value or death benefit unless you add riders that reduce the payout.

- Payout rates from FIA with GLWB are currently competitive with or better than SPIA rates for most ages and scenarios, while offering significantly more flexibility and beneficiary protection.

That said, we always run the numbers across all available options for each client situation. If a SPIA or DIA ever produces a meaningfully better outcome for a specific set of needs, we will say so. Right now, in the current rate environment, the FIA with GLWB wins in nearly every scenario we model. See our full comparison on the FIAs with GLWB vs. SPIA vs. DIA page.

The 10-Year Runway: Why Starting Early Dramatically Increases Your Income

One of the most powerful and underused strategies in retirement income planning is funding a FIA with GLWB up to 10 years before you need the income. During the deferral period, your income base grows at a contractually guaranteed rollup rate. The longer you wait to activate income, the larger your income base and the higher your monthly payment when you turn it on.

The difference between starting a PLI strategy at age 55 versus waiting until age 65 can nearly double your guaranteed monthly income from the same initial premium. This is the wholesale versus retail concept: the earlier you act, the more income you lock in for life. For a full breakdown of how the runway strategy works, see the 10-Year FIA + GLWB Runway Strategy page.

PLI Trade-Offs: What to Understand Before You Commit

No financial tool is perfect. Here is an honest look at the trade-offs you need to understand before choosing a PLI solution.

- Fees: Variable annuity PLI options can carry total annual fees of 2% to 4% or more, including mortality and expense charges, administrative fees, investment management fees, and income rider fees. Fixed indexed annuities with GLWB typically have lower fees, but the income rider cost still reduces your account value over time. It does not reduce your guaranteed income payments.

- Liquidity limits: Assets committed to a PLI strategy are not fully liquid. Most contracts allow penalty-free withdrawals of a percentage of the account value each year, but taking out more than the scheduled income can reduce your future guaranteed payments. This is why PLI is sized for essentials only, not your entire savings.

- Caps and participation rates: Fixed indexed annuities link growth to a market index but cap your upside through participation rates and caps that can change each year. The income base growth during deferral is typically guaranteed by contract regardless of index performance, but account value growth depends on index credits.

- Insurer strength: Guarantees are backed by the claims-paying ability of the issuing insurance company, not the government or the stock market. Always verify the financial strength ratings of any insurer you consider. State guaranty associations provide a limited safety net if an insurer fails, with coverage typically ranging from $100,000 to $250,000 per person per insurer per state. Check your state’s rules at nolhga.com.

Tax Treatment of PLI Income

How your PLI income is taxed depends entirely on how the annuity was funded.

- After-tax (non-qualified) dollars: Only the earnings portion of each payment is taxable. The portion representing your original principal is returned tax-free using the IRS exclusion ratio.

- Pre-tax dollars (traditional IRA or 401k): 100% of each payment is taxable as ordinary income, the same as any other withdrawal from a pre-tax account.

- Roth IRA or Roth 401k dollars: Income is completely tax-free, assuming the account meets the qualified distribution rules.

- Early withdrawals: Withdrawals before age 59 and a half may be subject to a 10% IRS penalty on the taxable portion in addition to ordinary income tax.

The funding source also affects your IRMAA exposure. Pre-tax PLI payments count toward your modified adjusted gross income and can trigger or increase Medicare surcharges. Roth-funded PLI payments do not. This is an important planning consideration when sizing your PLI strategy alongside your overall retirement income plan.

What the Research Shows About Guaranteed Income Floors

The case for building a guaranteed income floor is not just intuitive. It is backed by significant independent research.

- BlackRock: Retirees with a guaranteed income floor have, on average, 22% more potential spending power than those relying only on portfolio withdrawals. See the BlackRock whitepaper.

- EBRI 2024 Retirement Confidence Survey: 83% of workers in a workplace retirement plan are interested in guaranteed income products. See the EBRI survey.

- EBRI 2024 Spending Study: Retirees with guaranteed income report higher personal well-being and more positive spending outlooks compared to those relying on portfolio withdrawals. See the EBRI spending study.

The research consistently points to the same conclusion: guaranteed income does not just protect your finances. It changes how you experience retirement. Retirees with a guaranteed income floor spend more confidently, worry less, and report higher satisfaction with their retirement than those who depend entirely on portfolio withdrawals.

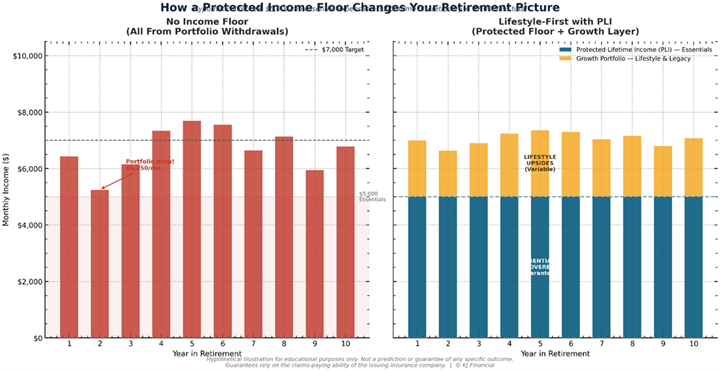

How a Protected Income Floor Changes Your Retirement Picture

Lifestyle-First Planning: PLI Only for What Must Happen

The most common misunderstanding about PLI is that it means putting all your money into an annuity. That is not how Lifestyle-First planning works. PLI is sized to cover only your essential expenses: housing, food, healthcare, utilities, and the non-negotiable experiences that matter most to you. Everything above that stays in growth assets where it can compound over time for upgrades, travel, gifts, and legacy.

This structure does something counterintuitive. Because your essentials are guaranteed, you actually become more comfortable taking appropriate risk with your growth assets. Many clients find they invest more confidently once their income floor is in place, because they know a market downturn cannot threaten their lifestyle. The income floor does not reduce your growth potential. It frees you to pursue it without fear.

Myths and Truths About Protected Lifetime Income

- Myth: Annuities are always too expensive to be worth it.

Truth: When sized correctly for your essentials, a FIA with GLWB produces more than double the monthly income of the traditional 4% rule while preserving your account value and a death benefit. The cost needs to be weighed against the guaranteed income it produces, not compared to holding cash. - Myth: All annuities are the same.

Truth: The differences between a variable annuity, a fixed indexed annuity, a SPIA, and a DIA are significant in terms of fees, payout rates, flexibility, and beneficiary protections. Comparing them carefully before choosing is essential. - Myth: If the insurance company fails, I lose everything.

Truth: State guaranty associations provide a limited safety net, typically $100,000 to $250,000 per person per insurer per state. Working with financially strong, highly rated insurers significantly reduces this risk. Check your state’s coverage at nolhga.com. - Myth: PLI income is always tax-free.

Truth: Tax treatment depends entirely on the funding source. Pre-tax funded PLI is fully taxable as ordinary income. After-tax funded PLI uses an exclusion ratio. Roth-funded PLI is tax-free. - Myth: Using PLI means I give up all growth potential.

Truth: PLI covers only your income floor. Everything above that stays in growth assets. Most clients find they invest more aggressively, not less, once their essentials are secured.

Pros and Cons of Using PLI for Your Income Floor

Pros:

- Guaranteed income for life regardless of market performance, interest rates, or longevity

- More than double the monthly income of the traditional 4% rule at current 2026 rates

- Account value and death benefit preserved for beneficiaries with FIA and GLWB structure

- BlackRock research supports 22% more potential spending power versus withdrawal-only strategies

- EBRI research links guaranteed income to higher well-being and more confident spending in retirement

- Frees growth assets to be invested more aggressively without fear of market downturns threatening essentials

Cons:

- Reduced liquidity compared to keeping all assets in a portfolio

- Fees, particularly on variable annuity options, can be significant

- Caps and participation rates on indexed options can change annually

- Guarantees depend on insurer financial strength, not government backing

- Not appropriate for every dollar or every goal, only for essential income floor sizing

- Difficult or impossible to exit once started without potential penalties or loss of guarantees

PLI Planning in Missouri, Florida, Kansas, Nebraska, and Iowa

State rules matter when selecting a PLI solution. Missouri, Florida, Kansas, Nebraska, and Iowa each have their own state guaranty association coverage limits, tax treatment rules for annuity income, and product availability. KJ Financial is licensed in all five states and evaluates PLI options through the lens of your specific state’s rules so you get the most appropriate solution for where you live and retire.

Summary

For most retirees who want guaranteed income covering their essential expenses, a fixed indexed annuity with a GLWB is the most effective and flexible tool available in 2026. It produces income rates that far exceed traditional withdrawal strategies, preserves your account value for beneficiaries, and allows you to defer income activation while your income base grows. The trade-offs are real and need to be understood, but for the specific job of securing an income floor that markets cannot touch, PLI does that job better than any alternative we have found. Always verify current rates, compare options across carriers, and confirm insurer financial strength before committing.

The bigger question behind all of this: lump sum or monthly paycheck? Here is that comparison in plain numbers, including what a MetLife study found about how long most lump sums actually last.

Frequently Asked QuestionsWhat is Protected Lifetime Income and how does it work?

Protected Lifetime Income is a guaranteed income stream that pays you a set amount every month for life, regardless of what markets do. It is backed by the claims-paying ability of the issuing insurance company, not the stock market. It is designed to cover your essential expenses so that market volatility can never force you to cut your core lifestyle.

What is a GLWB and why does it matter?

A Guaranteed Lifetime Withdrawal Benefit is a rider attached to a fixed indexed annuity that guarantees you can withdraw a set percentage of a protected income base for life, even if your account value drops to zero. Your income base often grows at a guaranteed rollup rate during the deferral period, which is why starting earlier produces significantly more income. Unlike a SPIA, a GLWB preserves your remaining account value as a death benefit for your beneficiaries.

How does a FIA with GLWB compare to a SPIA or DIA?

In most 2026 scenarios, a FIA with GLWB produces equal or higher income than a SPIA while preserving account value and flexibility. A SPIA pays immediately but surrenders your principal with no remaining death benefit on a life-only option. A DIA allows deferral like a FIA but also surrenders principal. We always run all three options for each client situation, and right now the FIA with GLWB wins in nearly every case.

What is the 10-year runway strategy and why does starting early matter so much?

Funding a FIA with GLWB up to 10 years before you need the income allows your income base to grow at a guaranteed rollup rate during the deferral period. The result is significantly higher guaranteed monthly income when you activate it compared to starting at retirement. Starting at age 55 versus waiting until age 65 can nearly double your guaranteed monthly income from the same premium. Time is the most powerful factor in maximizing PLI income.

Are annuities safe? What are the real pros and cons?

Annuities are backed by the financial strength of the issuing insurance company, not the government or the stock market. Working with highly rated insurers significantly reduces risk. State guaranty associations provide limited protection if an insurer fails, typically $100,000 to $250,000 per person per insurer per state. The pros are guaranteed income, death benefit preservation with GLWB, and higher withdrawal rates than traditional portfolio strategies. The cons are reduced liquidity, fees, and the need to select a financially strong insurer.

What is Lifestyle-First Retirement Income Planning?

Lifestyle-First planning starts with your life and income needs rather than a portfolio balance or withdrawal rate. Essential expenses and non-negotiable experiences are covered by Protected Lifetime Income first. Growth assets handle everything above that. PLI is sized only for your income floor, freeing the rest of your savings to be invested for growth, flexibility, and legacy.

How does PLI protect against sequence of returns risk?

Because PLI covers your essential expenses with guaranteed income, a market downturn cannot force you to sell growth assets at a loss to pay your bills. Your income floor is secure regardless of what markets do. This means your growth assets can stay invested through downturns and benefit from recoveries without being depleted at the worst possible time.

Does PLI protect against inflation?

PLI with a fixed payment provides stable income that does not automatically adjust for inflation. However, the spending smile concept means your fixed PLI income often functions as an effective inflation hedge through your Slow-Go years when spending naturally declines. Some PLI solutions include cost-of-living adjustment riders that increase income over time, typically at a lower starting payout. Growth assets in the second layer of your plan are positioned to outpace inflation over the long term.

How do Roth conversions affect PLI income and taxes?

Roth-funded PLI income is completely tax-free and does not count toward your modified adjusted gross income for IRMAA purposes. Pre-tax funded PLI is fully taxable and can trigger or increase Medicare surcharges. Strategic Roth conversions before PLI income begins can significantly reduce your lifetime tax burden and keep your Medicare premiums lower.

Does PLI income trigger Medicare IRMAA surcharges?

It depends on how the annuity was funded. Pre-tax PLI income counts as ordinary income and can push you into higher IRMAA brackets, raising your Medicare Part B and Part D premiums. After-tax PLI income is partially taxable using the exclusion ratio. Roth-funded PLI income does not count toward MAGI and does not affect IRMAA at all.

How does PLI income compare to the 4% rule?

The traditional 4% rule produces approximately $333 per month per $100,000 invested. A FIA with GLWB at current 2026 rates produces approximately $640 per month per $100,000 for a couple and $690 for a single at age 65. That is nearly double the income, with the additional advantage that the PLI income is guaranteed for life regardless of market performance, while the 4% rule depends entirely on markets cooperating.

Does Missouri tax PLI income or Social Security?

As of 2026, Missouri fully exempts Social Security benefits from state income tax. PLI income funded with pre-tax dollars is taxable as ordinary income at both the federal and Missouri state level. PLI funded with after-tax or Roth dollars may have more favorable tax treatment depending on the funding source.

Does Florida tax PLI income or Social Security?

Florida has no state income tax, so Social Security, PLI income, and investment income are all free from state taxation. This makes Florida one of the most favorable states for building and receiving Protected Lifetime Income.

Does Nebraska tax PLI income or Social Security?

As of tax year 2025, Nebraska fully exempts all Social Security benefits from state income tax with no income thresholds. PLI income funded with pre-tax dollars remains taxable at both the federal and Nebraska state level depending on the funding source.

Does Kansas tax PLI income or Social Security?

Kansas exempts Social Security for residents with federal AGI of $75,000 or less. PLI income funded with pre-tax dollars is taxable as ordinary income and counts toward that AGI threshold, which is an important planning consideration for Kansas retirees sizing their PLI strategy.

Does Iowa tax PLI income or Social Security?

Iowa does not tax Social Security for residents age 55 or older and also exempts most qualifying retirement income for eligible taxpayers. PLI income tax treatment in Iowa depends on the funding source and whether it qualifies as exempt retirement income under Iowa law.

Experience: Kurt H. Jackson has spent more than 16 years evaluating, designing, and implementing Protected Lifetime Income strategies for retirees and pre-retirees across Missouri, Nebraska, Kansas, Iowa, and Florida. He has worked directly with clients who were skeptical of annuities, clients who had been sold the wrong product by someone else, and clients who discovered that a correctly sized FIA with GLWB transformed their retirement from one built on market hope to one built on guaranteed income. Before founding KJ Financial, he spent 20 years as a Certified Mortgage Planner working with more than 1,000 clients on complex financial decisions, giving him a deep understanding of how major financial commitments affect real families over time.

Expertise: Kurt is a Retirement Lifestyle Architect and the creator of the Lifestyle-First Retirement Income Planning framework. He specializes in evaluating PLI solutions across carriers, comparing FIA with GLWB against SPIA and DIA options, sizing income floors correctly for each client’s essential expenses, and integrating PLI with Roth conversion strategies, IRMAA management, and coordinated withdrawal planning. He is Life and Health Insurance Licensed in MO, NE, KS, IA, and FL. His practice focuses exclusively on insurance-based, tax-optimized retirement income strategies. He does not manage investments or sell securities.

Authoritativeness: Kurt founded KJ Financial and operates MaxMyRetirementIncome.com as a dedicated educational resource for retirees. His approach to PLI is grounded in independent research from BlackRock, EBRI, and academic retirement income researchers, applied to the practical income planning decisions his clients face. He publishes current 2026 payout rate data, transparent fee disclosures, and honest trade-off analysis so retirees can make informed decisions rather than being sold a product they do not fully understand.

Trustworthiness: KJ Financial is a compliance-first firm. All payout rates are presented as illustrative and subject to change before contract lock-in. Kurt H. Jackson is not a securities broker, registered investment advisor, or CPA. He does not receive commissions from recommending one carrier over another in an advisory context. Guarantees rely on the claims-paying ability of the issuing insurance company. State guaranty association coverage is limited and varies by state. Always verify coverage at nolhga.com.

Contact KJ Financial:

1014 E. 5th St., Maryville, MO 64468

Direct: 816.582.5532

Email: [email protected]

Website: www.MaxMyRetirementIncome.com

Educational only. Not tax, legal, or individualized investment advice. Guarantees rely on the issuing insurer’s claims-paying ability. Payout rates shown are illustrative as of April 2026 and are subject to change before contract lock-in. Any figures shown may differ for your situation based on age, health, product features, fees, allocations, and market conditions. For state guaranty association coverage details, visit nolhga.com.