Medicare Advantage vs. Medigap 2026: Costs, Coverage, Pros and Cons

Medicare Advantage plans typically offer lower monthly premiums but require you to use provider networks and can expose you to significant out-of-pocket costs in a bad health year. Medigap plans cost more each month but give you access to any Medicare-accepting provider nationwide, predictable costs, and meaningful travel coverage. The right choice depends on your health, how much you travel, your doctors, and how much cost uncertainty you can absorb. Lifestyle-First planning builds your Medicare costs into your income plan from the start so your choice fits your real retirement life.

Why Your Medicare Decision Matters More Than Most People Realize

Most retirees spend more time choosing a car than choosing a Medicare plan. That is a costly mistake. The plan you choose at 65 shapes your healthcare access, your out-of-pocket exposure, and your ability to see the doctors you want for the rest of your retirement. And in most states, if you choose Medicare Advantage and later want to switch to Medigap, you can be denied coverage or charged significantly higher premiums based on your health history. Getting this decision right from the start matters.

Fidelity estimates a 65-year-old couple retiring in 2026 will need approximately $330,000 for healthcare costs in retirement, not including long-term care. That number does not include IRMAA surcharges, which can add hundreds of dollars per month if your income is not managed carefully. Understanding your Medicare options is not just a healthcare decision. It is a retirement income decision.

Original Medicare: The Foundation

Original Medicare (Parts A and B) covers hospital and medical care but leaves you responsible for approximately 20% of costs with no annual out-of-pocket maximum. A major illness or surgery could cost you tens of thousands of dollars out of pocket with no cap. That gap is why virtually every retiree needs either a Medigap plan or a Medicare Advantage plan to limit their financial exposure.

What Is Medigap (Medicare Supplement)?

Medigap plans, also called Medicare Supplement plans, fill most or all of the cost gaps left by Original Medicare. You pay a monthly premium and in return your out-of-pocket costs become highly predictable. The two most popular Medigap plans in 2026 are Plan G and Plan N.

- Plan G: Estimated $100 to $250 per month for a 65-year-old, depending on location and insurer. Covers virtually everything Original Medicare does not, except the Part B deductible ($257 in 2026). After that deductible, your costs are essentially zero for covered services.

- Plan N: Estimated $80 to $200 per month. Lower premium than Plan G, with small co-pays for office visits and emergency room visits that do not result in admission.

- Both plans let you see any doctor or hospital that accepts Medicare, anywhere in the country, with no networks and no referrals required.

- Most Medigap plans include 80% coverage for emergency care abroad after a $250 deductible, up to a $50,000 lifetime limit. This is a meaningful advantage if you travel internationally.

- Critical timing point: You have a 6-month guaranteed issue window starting when you enroll in Part B at age 65. During this window, no insurer can deny you or charge you more based on health history. After this window closes, most states allow medical underwriting, meaning you could be denied or priced out of Medigap entirely if your health has changed.

What Is Medicare Advantage (Part C)?

Medicare Advantage plans are offered by private insurers approved by Medicare. They combine hospital, medical, and usually prescription drug coverage into a single plan and are required to cover at least everything Original Medicare covers.

- Many plans have $0 or very low monthly premiums, which makes them attractive upfront.

- Instead of a monthly premium, you pay co-pays and coinsurance each time you use care. Costs can add up quickly with frequent doctor visits or a serious health event.

- Plans use provider networks. You are typically required to use doctors, hospitals, and facilities in your plan’s network, and HMO plans usually require referrals to see specialists.

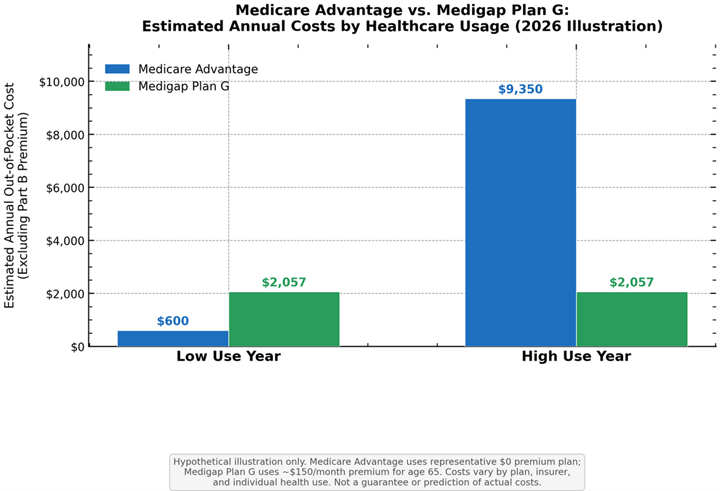

- The annual out-of-pocket maximum (MOOP) for 2025 was $9,350 for in-network care and $14,000 for combined in- and out-of-network PPO care. The 2026 MOOP is expected to be modestly higher.

- Benefits, premiums, co-pays, and networks can all change every year at open enrollment. A plan that works well today may look very different next year.

- Routine care outside your plan’s service area is generally not covered. Emergency care is always covered nationwide.

Medicare Advantage vs. Medigap: Side-by-Side Comparison 2026

| Feature | Medicare Advantage | Medigap Plan G |

|---|---|---|

| Monthly Premium | Often $0 to $50 | $100 to $250 (varies by age, location, insurer) |

| Annual Out-of-Pocket Maximum | $9,350+ in-network (2025); higher expected in 2026 | Essentially $0 after the $257 Part B deductible |

| Provider Choice | Network-limited; referrals often required | Any Medicare-accepting provider nationwide |

| Prescription Drug Coverage | Usually included | Must add a separate Part D plan |

| Dental, Vision, Hearing | Often included but can change yearly | Not included |

| International Travel Coverage | Emergency only, no routine care abroad | 80% of emergency care abroad up to $50,000 lifetime after $250 deductible |

| Cost Predictability | Variable based on how much care you use | Highly predictable |

| Switching Flexibility | Can switch annually at open enrollment | Guaranteed issue at 65 only; medical underwriting applies after that in most states |

Prescription Drug Coverage and Part D IRMAA

Most Medicare Advantage plans include prescription drug coverage. If you choose Original Medicare plus a Medigap plan, you will need to add a stand-alone Part D plan for drugs.

In 2026, the annual out-of-pocket cap for Part D drugs is $2,100. If your income exceeds certain thresholds, you will also pay a Part D IRMAA surcharge on top of your plan premium. For 2026, Part D IRMAA starts at $14.50 per month for single filers with modified adjusted gross income over $109,000. This surcharge applies regardless of whether you have Medicare Advantage or Medigap. Managing your taxable income is important for both. See What Is IRMAA and Why Does It Matter for the full 2026 bracket breakdown.

Medicare Advantage vs. Medigap Cost Comparison

Myths and Truths About Medicare Advantage and Medigap

- Myth: Medicare Advantage is always cheaper than Medigap.

Truth: The monthly premium is often lower, but your total annual costs can be significantly higher in a year with serious illness or surgery due to co-pays and coinsurance that can reach the full MOOP. - Myth: Medigap covers everything so I will never have out-of-pocket costs.

Truth: You still pay your monthly premium and the Part B deductible ($257 in 2026 for Plan G). Dental, vision, and hearing are not included. - Myth: I can always switch from Medicare Advantage to Medigap later if I want to.

Truth: After the 6-month guaranteed issue window at age 65, most states allow insurers to deny your Medigap application or charge higher premiums based on your health history. Waiting can close that door permanently. - Myth: Medicare Advantage covers me anywhere in the country.

Truth: Emergency care is always covered. Routine care outside your plan’s service area typically is not, which can be a serious problem if you spend time in multiple states or travel frequently. - Myth: The dental and vision benefits that come with Medicare Advantage are guaranteed long-term.

Truth: These benefits can be reduced, changed, or eliminated at every annual open enrollment. They are not guaranteed features of your coverage going forward. - Myth: Medigap offers no coverage outside the United States.

Truth: Most Medigap plans cover 80% of emergency care abroad after a $250 deductible, up to a $50,000 lifetime maximum. For retirees who travel internationally, this is a significant advantage Advantage plans do not offer.

How to Choose: The Right Questions to Ask

The decision between Medicare Advantage and Medigap is not purely financial. It is a lifestyle decision. Here are the questions that matter most:

- Do you travel frequently or split time between states? Medigap’s nationwide provider access and international emergency coverage make it the stronger choice for active travelers.

- Do you have specific doctors or specialists you want to keep? Medigap lets you see any Medicare-accepting provider without network restrictions or referrals.

- Can your budget absorb a bad health year? If a $9,000 or more out-of-pocket year would create financial stress, Medigap’s predictability is worth the higher monthly premium.

- Are you in good health and staying local? Medicare Advantage can work well if you are healthy, use in-network providers regularly, and value the lower premium and extra benefits.

- What is your IRMAA exposure? Both plans are subject to IRMAA surcharges if your income is above the thresholds. Managing your taxable income through Roth conversions and coordinated withdrawals matters regardless of which plan you choose.

Lifestyle-First planning integrates your Medicare costs into your income floor from the beginning. When your healthcare expenses are part of your Protected Lifetime Income plan, you are never caught off guard by a premium increase or an unexpected medical bill.

Medicare Planning in Missouri, Florida, Kansas, Nebraska, and Iowa

State rules affect your Medicare options in meaningful ways. Missouri, Florida, Kansas, Nebraska, and Iowa each have their own regulations around Medigap pricing methods, guaranteed issue rights, and open enrollment protections. Some states provide additional consumer protections beyond federal minimums. KJ Financial is licensed in all five states and can help you understand your options and avoid costly timing mistakes wherever you plan to retire.

Key Takeaways

- Original Medicare leaves you with unlimited out-of-pocket exposure. Every retiree needs either Medigap or Medicare Advantage to cap that risk.

- Medicare Advantage offers lower or $0 premiums but comes with networks, managed care rules, variable costs, and benefits that can change yearly.

- Medigap costs more monthly but delivers nationwide provider access, predictable expenses, and meaningful international emergency coverage.

- The 6-month guaranteed issue window at age 65 is often your only chance to enroll in Medigap without medical underwriting in most states. Do not miss it.

- IRMAA surcharges apply to Medicare costs regardless of which plan you choose. Managing your taxable income is essential for both options.

- Fidelity estimates a couple retiring in 2026 will need approximately $330,000 for retirement healthcare costs, not including long-term care. Build these costs into your income plan from day one.

Frequently Asked Questions

What is IRMAA and how does it affect my Medicare premiums?

IRMAA is a Medicare income-related surcharge added to your Part B and Part D premiums when your modified adjusted gross income exceeds certain thresholds. In 2026, a single filer with income over $109,000 sees their Part B premium jump from $202.90 to $284.10 per month. IRMAA applies to both Medicare Advantage and Medigap enrollees and is calculated using your tax return from two years prior. A spike in income from an RMD, a Roth conversion, or an investment sale can trigger IRMAA surcharges two years later even if your income returns to normal.

How can Roth conversions help me avoid Medicare IRMAA surcharges?

Roth conversions move money from traditional IRAs or 401(k)s into a Roth IRA. Future Roth withdrawals are tax-free and do not count toward your modified adjusted gross income. Done strategically in the years before RMDs begin, Roth conversions reduce your future taxable income and can help you stay below IRMAA thresholds permanently, keeping your Medicare premiums lower for the rest of your retirement.

How do Required Minimum Distributions affect my Medicare costs?

RMDs from traditional IRAs and 401(k)s count as ordinary income and increase your modified adjusted gross income, which is what Medicare uses to calculate IRMAA surcharges. A large RMD can push you into a higher IRMAA bracket and add hundreds of dollars per month to your Medicare premiums, even if you do not need or want that income. Proactive Roth conversion planning before RMDs begin is one of the most effective ways to reduce this exposure.

When should I claim Social Security and how does it interact with Medicare?

Claiming Social Security at 65 can trigger automatic Medicare Part A enrollment. The timing of your Social Security claim also affects your income level, which in turn affects IRMAA surcharges two years down the road. Coordinating your Social Security claiming strategy with your Medicare enrollment timing and your overall income plan is an important part of Lifestyle-First retirement planning.

What is guaranteed retirement income and how does it fit into Medicare planning?

Protected Lifetime Income gives you a steady, predictable monthly income stream. When your essential expenses, including Medicare premiums and expected out-of-pocket costs, are covered by guaranteed income rather than market-dependent withdrawals, healthcare costs become a manageable, budgeted expense rather than a source of financial anxiety in retirement.

What is a smart withdrawal strategy that helps manage Medicare costs?

A smart withdrawal strategy coordinates income from Roth accounts, traditional accounts, and Protected Lifetime Income to keep your modified adjusted gross income below IRMAA thresholds whenever possible. For a married couple, this can save thousands of dollars per year in Medicare surcharges without any reduction in their lifestyle or spending.

Can Protected Lifetime Income help cover healthcare costs in retirement?

Yes. A well-designed Protected Lifetime Income strategy can include your projected Medicare premiums and expected out-of-pocket costs as part of your income floor. When healthcare is built into your guaranteed income, you are never dependent on market performance to pay your medical bills.

Does Missouri tax Social Security, and how does that affect Medicare planning?

As of 2026, Missouri fully exempts Social Security benefits from state income tax with no income limits. This means Social Security income does not increase your Missouri state tax burden, which can help you manage your overall income level and stay below federal IRMAA thresholds.

Does Florida tax Social Security, and how does that affect Medicare planning?

Florida has no state income tax, so Social Security, pension income, IRA withdrawals, and Protected Lifetime Income payments are all completely exempt from state taxation. This gives Florida retirees significant flexibility to manage their modified adjusted gross income and reduce IRMAA exposure compared to retirees in higher-tax states.

Does Nebraska tax Social Security, and how does that affect Medicare planning?

As of tax year 2025, Nebraska fully exempts all Social Security benefits from state income tax with no income thresholds or phase-outs. This makes income planning for IRMAA management more straightforward for Nebraska retirees and removes one variable from the tax equation.

Does Kansas tax Social Security, and how does that affect Medicare planning?

Kansas fully exempts all Social Security benefits from state income tax for every resident effective tax year 2024, with no income threshold. The state exemption is now automatic for Kansas retirees regardless of income, but careful withdrawal sequencing and income planning still matters for managing federal IRMAA exposure on your Medicare premiums.

Does Iowa tax Social Security, and how does that affect Medicare planning?

Iowa does not tax Social Security for residents age 55 or older. Iowa also exempts most other qualifying retirement income, including pensions, IRAs, and annuities, for eligible taxpayers. This gives Iowa retirees meaningful flexibility in managing their taxable income and staying below IRMAA thresholds.

Experience: Kurt H. Jackson has spent more than 16 years helping retirees and pre-retirees across Missouri, Nebraska, Kansas, Iowa, and Florida navigate Medicare decisions as part of a broader Lifestyle-First retirement income plan. He has worked with clients who chose Medigap for travel flexibility and nationwide provider access, clients who chose Medicare Advantage for lower premiums and bundled benefits, and clients who missed their guaranteed issue window and faced difficult underwriting situations as a result. That real-world experience shapes how he integrates Medicare costs into every retirement income plan from day one.

Expertise: Kurt is a Retirement Lifestyle Architect and the creator of the Lifestyle-First Retirement Income Planning framework. He specializes in building Medicare costs, IRMAA management, and healthcare budgeting into retirement income plans alongside Protected Lifetime Income design, Roth conversion strategies, and coordinated withdrawal planning. He is Life and Health Insurance Licensed in MO, NE, KS, IA, and FL. His practice focuses exclusively on insurance-based, tax-optimized retirement income strategies. He does not manage investments or sell securities.

Authoritativeness: Kurt founded KJ Financial and operates MaxMyRetirementIncome.com as a dedicated educational resource for retirees in Missouri and surrounding states. His Lifestyle-First framework treats Medicare as an income planning decision, not just a healthcare decision, connecting plan choice to IRMAA exposure, withdrawal strategy, Roth conversion timing, and Protected Lifetime Income design in a way that most retirees have never seen before.

Trustworthiness: KJ Financial is a compliance-first firm. All figures presented on this page are illustrative and hypothetical. Kurt H. Jackson is not a securities broker, registered investment advisor, or CPA. He does not sell Medicare Advantage or Medigap plans. His guidance on Medicare is educational and income-planning focused. For Medicare plan enrollment, always work with a licensed Medicare broker or contact Medicare directly at medicare.gov.

Contact KJ Financial:

1014 E. 5th St., Maryville, MO 64468

Direct: 816.582.5532

Email: [email protected]

Website: www.MaxMyRetirementIncome.com

Educational only. Not tax, legal, or individualized insurance advice. Guarantees rely on the issuing insurer’s claims-paying ability. Any figures shown are illustrative and may differ for your situation based on age, health, location, plan features, and individual use. For the latest Medicare rules and plan details, visit medicare.gov.